Coal sections of Least Cost Power Development Plan 2017–2037

Official government LCPDP

LCPDP updated June 2018. Authors: Republic of Kenya, Energy Regulatory Commission, Geothermal Development Company, KenGen, Kenya Power, Rural Electrification Authority, KETRACO (Kenya Electricity Transmission Co.), KNEB (Kenya Nuclear Electricity Board)

The report is available on the Geothermal Association of Kenya website. Until mid-2019, the report PDF was still available on the ERC (now called EPRA) website, but now is listed as page not found. Much earlier, it had been taken down from the list of documents at the ERC (and originally marked 2017–2022) and thus shows an error.

It will remain available here for reference as well:

LCPDP Sections on Coal

Expansion planning: Coal to increase from 0 to 19.5% of total installed capacity.

Key observation arising from the expansion plan:

(ii) Addition of 981.5 MW Lamu coal plant in 2024 will aggravate the projected supply-demand imbalance as the surplus margin would surpass 1,500 MW being 43% above the sum of peak and required reserve, with 32% excess energy during the year. The system LEC [levelised electricity cost] would rise rapidly to reach Shs. 16.86/kWh by the year 2024.

(iii) Capacity factors for geothermal, hydro and coal plants average 71.7%, 44.9% and 0.9% over the period after 2019, implying that the power plants, and particularly Lamu coal, will be grossly underutilized should demand grow moderately.

Recommendations:

Arising from this study, the following are recommended as necessary to ensure effective implementation and address implementation concerns highlighted in the study

a) Renegotiate PPAs for large power plants, to introduce operation flexibility, reduce reserve requirements and optimize energy costs.

xvi. and xvii.

Lamu coal plant listed as coming board in 2024, as in the below chart:

4. ASSESSMENT OF NATURAL ENERGY RESOURCES IN KENYA

At present, coal is the only domestic fossil energy resource available for extraction and potential use in power generation.

4.1.4. Solid fuels

4.1.4.1. Coal

Coal is a solid fossil fuel consisting mainly of carbon, i.e. organic matters, and differing quantities of other substances such as minerals, sulphur or water. It is found in and extracted from geological formations beneath the earth’s surface. For utilization in power plants, coal can be distinguished by the heating value and its composition ranging from lignite with a relatively low heating value to sub-bituminous coal. Coal has been the second most important fossil energy source in the world measured by energy content behind crude oil4. It is the most important fuel for power generation worldwide due to its abundant reserves, which are distributed relatively evenly among many countries. However, the use of coal is accompanied by strong environmental impacts, such as high emissions of sulphur dioxide, heavy metals and harmful greenhouse gases.

In Kenya local coal reserves can be found in the Mui Basin which runs across the Kitui county 200 km east of Nairobi. The coal basin stretches across an area of 500 square kilometers and is divided into four blocks: A (Zombe — Kabati), B (Itiku — Mutitu), C (Yoonye — Kateiko) and D (Isekele — Karunga). Coal of substantial depth of up to 27 meters was discovered in the said basin. 400 million tons of coal reserves were confirmed in Block C109. The Government of Kenya has awarded the contract for mining of coal in Blocks C and D. Coal mining, in particular open pit as planned for Mui basin, has strong environmental and social impacts. The mining will require large scale resettlement plans. Further, mining will produce considerable pollution. The local coal are of lower quality compared to imported coal from South Africa with regard to content of energy, ash, moisture and sulphur5.

Due to its widespread deposits, production experience as well as relatively low costs, coal is an important fuel option for expansion planning but the negative environmental impacts has to be factored in. The planned Lamu power plant would be the first coal power plant in Kenya. Coal power plant based on domestic coal could be developed directly near the Mui Basin in Kitui County once the mine is developed.

4.1.5. Renewable energy sources

Kenya has promising potential for power generation from renewable energy sources. Abundant solar, hydro, wind, biomass and geothermal resources led the government to seek the expansion of renewable energy generation in the country. Following a least cost approach, the government has prioritized the development of geothermal and wind energy plants as well as solar-fed mini-grids for rural electrification.

4.1.5.1. Geothermal energy

Kenya is endowed with geothermal resources, mainly in the Rift Valley as shown in figure 2. Geothermal energy has comparably low electricity production costs. Currently, geothermal capacity provide nearly 50% of total power generation. The current total geothermal installed capacity amounts to nearly 650 MW. The KenGen power plants are equipped with single flash steam technology while the remaining capacity owned and operated by independent power producers (IPP) use binary steam cycle technology. Due to the low short-run marginal costs, geo- thermal power plants generally run as base load.

… Kenya geothermal resource potential is estimated at 10,000 MW along the Kenyan Rift Valley.

5.3.2. Coal price forecast

The first coal power plant in Kenya is expected to be in operation in the year 2024 running on imported coal until local deposits are exploited. South Africa is the likely choice of imported coal due to their proximity to the Mombasa Port compared to other export terminals. South Africa is the world’s fifth-largest coal producer and has historically been mainly exporting coal to the European market but lately increased exports to Asian countries. Other African countries, besides South Africa, expected to play an emerging role in coal trade are Botswana, Mozambique and Tanzania. The World Bank reports average coal prices in South Africa rose to US$81.9/t in 2017 from 64.1/t in 2016 and stood at US$92.7 in December 2017. Australian coal prices rose to US$88.4/t from US$65.9/t in the corresponding period.

The World Oil Outlook 2016 by OPEC predicts that global coal demand will increase gradually by an average rate of 0.6% p.a up to 2040. The report attributes the high increase in coal prices at the end of 2017 to a surge in power demand in China and supply issues in some major exporters.

In the reference forecast of this study, the base price of US$81.9/t has been used on the basis of price movements alongside oil and natural gas prices. Coal prices are projected to rise to US$100 in 2020 to US$108/t in 2040. A high price forecast of US$102/t in 2020 is projected, rising to US$122.4/t and US$129.6/t in 2030 and 2040, respectively.

… In the long-term, however, the introduction of environmental policies should favour gas development versus coal.

5.4.1. Tecno-Economic data for candidate projects

Input data sets for the various candidates considered are presented below grouped under four categories:

a) Fuel switching fossil thermal candidates b) Fossil fuel thermals and nuclear

c) Wind, solar, bagasse and geothermal

d) Hydropower

The renewables considered include solar, wind and biogas…

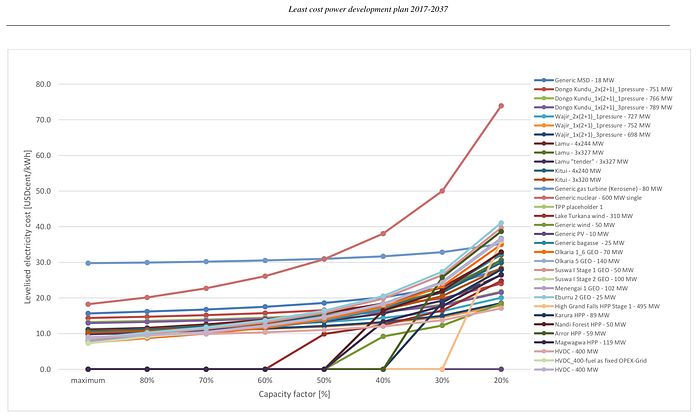

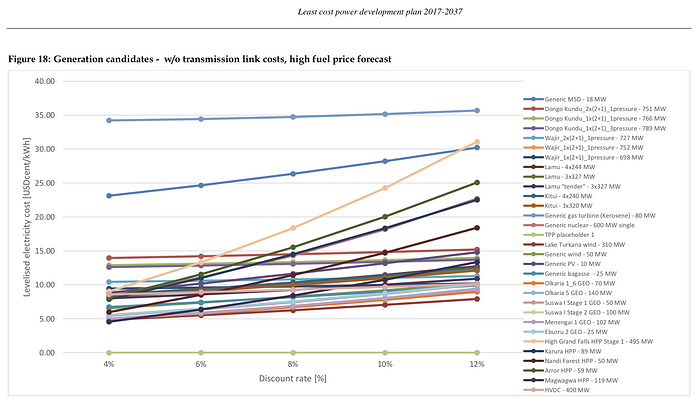

When ranking technologies against discount factors, the Levelized costs changes on these factors but the outstanding feature is that Geothermal, wind, hydro, and biomass plants are competitive while nuclear, coal, medium speed diesels, and Natural gas technologies remain uncompetitive irrespective of the discount factor applied.

The results however reveal critical energy planning information as follows:

- MSDs, natural gas and hydros are good for peaking

- Geothermal will remain the most competive technology with respect to development of base load capacity in the medium to long term

- Plants with a significant fuel cost charge are not preffered for base load expansion due to their relatively high variable costs

Table 25: Technical and cost data for candidate fossil fuel and nuclear plants

Lamu 3x327MW, Lamu coal plant, TPP9

2.3 Fuel and efficiency:

Primary fuel coal

Price level transport cost cif

Net calorific value (effective fuel) 21.0 MJ/kg

Costs effective fuel (actual simulation year) 4.2 USD/GJ

Max efficiency 41%

Specific fuel consumption (at max efficiency) 414.1 kg/MWh

Specific field costs (at max efficiency) 36.8 USD/MWh

2.4 Capacity:

Unit Type 1 ST, Capacity installed (gross) 1069.5 MW

Maximum capacity available (net) 981.8 MW

2.5 Generation (net):

Average future generation 6,450.1 GWh/a

Effective available generation (thermal) 7,463.3 GWh/a

Average future capacity factor 75%

2.6 Availability:

Effective available capacity factor (thermal) 87%

Forced Outage Rate (FOR) 5%

Planned Outage Rate (POR) 25 days/year

2.7 Lifetime & Construction:

Lifetime total (expected) 30 years

1st year of operation open

Last year of operation (latest) na

2.8 Costs:

O&M Fixed:

68.1 USD/kW/year & 66,831.3 TUSD/year & 3% of CAPEX

O&M Variable: 1.6 USD/MWh

O&M Total: 3% % of CAPEX

Specific Fuel Costs (at max efficiency) 36.8 USD/MWh

Inland fuel transport costs 0.0 USD/GJ

(note: zero listed for all plants)

Average Generation Costs (fuel + O&M variable): 38.1 USD/MWh

Investment Costs Plant:

TOTAL Investment Costs 2,506.0 MUSD

Specific investment costs 2,552.5 USD/kW

Residual value (HPP 60% of civil works) 0% of CAPEX

Civil works cost share na

2.9 Net Heat Rate at load (TPP):

100% 8,695.2

90% 8,707.2

80% 8,772.4

70% 8,898.9

60% 9,073.7

50% 9,336.3

40% 9,748.1

30% 10,419.0

20% 11,165.7

Kitui 3x320 MW, Kitui coal plant, TPP13

2.3 Fuel and efficiency:

Primary fuel coal

Price level transport cost fob

Net calorific value (effective fuel) 21.0 MJ/kg

Costs effective fuel (actual simulation year) 3.9USD/GJ

Max efficiency 37%

Specific fuel consumption (at max efficiency) 458.3 kg/MWh

Specific field costs (at max efficiency) 37.5 USD/MWh

2.4 Capacity:

Unit Type 1 ST

Capacity installed (gross) 1058.2 MW

Maximum capacity available (net) 972.4 MW

2.5 Generation (net):

Average future generation 6,388.5 GWh/a

Effective available generation (thermal)7,391.9 GWh/a

Average future capacity factor 75%

2.6 Availability:

Effective available capacity factor (thermal) 87%

Forced Outage Rate (FOR) 5%

Planned Outage Rate (POR) 30 days/year

2.7 Lifetime & Construction:

Lifetime total (expected) 30 years

1st year of operation open

Last year of operation (latest) na

2.8 Costs:

O&M Fixed:

69 USD/kW/year & 67,093.4 TUSD/year & 3% of CAPEX

O&M Variable: 1.4 USD/MWh

O&M Total: 3% % of CAPEX

Specific Fuel Costs (at max efficiency) 37.5 USD/MWh

Inland fuel transport costs 0.0 USD/GJ

(note: zero listed for all plants)

Average Generation Costs (fuel + O&M variable): 38.9 USD/MWh

Investment Costs Plant:

TOTAL Investment Costs 2,360.6 MUSD

Specific investment costs 2,427.7 USD/kW

Residual value (HPP 60% of civil works) 0% of CAPEX

Civil works cost share na

2.9 Net Heat Rate at load (TPP):

100% 9,624.6

90% 9,577.9

80% 9,608.3

70% 9,721.1

60% 9,899.8

50% 10,145.3

40% 10,517.6

30% 11,130.5

20% 11,813.4

Table 32: Long Term Planting Sequence-Reference scenario

Plant characteristics: ID, PP name, PP group, Fuel, Net capacity MW, Use plant, Plant expansion status in base year, COD

u23 Lamu Unit 1 Coal Coal imported 327 yes obligatory candidate 2024

u24 Lamu Unit 2 Coal Coal imported 327 yes obligatory candidate 2024

u25 Lamu Unit 3 Coal Coal imported 327 yes obligatory candidate 2024

[excluding various other charts with different forecasts]

6.7. Conclusions

6.7.1. Fixed System expansion case

(ix) Addition of 981.5 MW Lamu coal plant in 2024 will aggravate the projected supply-demand imbalance as the surplus margin would surpass 1,500 MW being 43% above the sum of peak and required reserve, with 32% excess energy during the year. The system LEC would rise rapidly to reach Shs. 16.86/kWh by the year 2024.

(x) Capacity factors for geothermal, hydro and coal plants average 71.7%, 44.9% and 0.9% over the period after 2019, implying that the power plants, and particularly Lamu coal, will be grossly underutilized should demand grow moderately.

(xi) Lower demand would worsen the system LEC and plant utilization levels while higher demand would improve the two parameters.

6.7.2. Optimised expansion plan

(ii) With model given the opportunity to optimise the expansion plan, the first unit of coal is selected is Kitui 320MW coal added 2029. The next coal unit would be Lamu 327MW in 2034 followed by 320 Kitui coal unit in 2035 and another 327MW Lamu unit in 2036.

(iii) The excess capacity would reduce from an average of 398MW between 2019 and 2023 to an average of 80MW of the rest of the planning period.

The system LEC would rise gently to reach Shs. 12.45/kWh by the year 2022 and stabilize to an average of Shs. 11.07/kWh over the rest of the planning period.(iv) Capacity factors for geothermal, hydro and coal plants average 77.8%, 30.0% and 24.7% over the period 2019–2037, implying that the power plants and particularly the Lamu coal plant will be grossly underutilized.

Lower demand would worsen the system LEC and plant utilization levels while higher demand would improve the two parameters.

6.7.3 Fixed Medium-term case

(i) Implementation of all committed projects by 2024 would raise the existing capacity to 3,538 MW resulting in an average of 709 MW excess capacity with demand growing moderately according to the reference forecast.

(ii) Addition of 981.5 MW Lamu coal plant in 2024 aggravates the projected supply-demand imbalance as the excess capacity would be 1,362 MW being 39% above the sum of peak and required reserve, with 29% excess energy during the year. The system LEC would rise rapidly to reach Shs. 16.25/kWh by the year 2024.

(iii) Capacity factors for geothermal, hydro and coal plants average 75.5%, 44.3% and 6.3% over the period 2019–2037, implying that some power plants, especially the Lamu coal plant, will be grossly underutilized.

(iv) Lower demand would worsen the system LEC and plant utilization levels while higher demand would improve the two parameters.

6.8. Recommendations

The following recommendations are derived based on the generation expansion planning analyses carried out.

(i) Renegotiate the PPAs for large power plants such as Ethiopia HVDC and Lamu Coal to introduce operation flexibility and minimize energy costs.

(ii) Implementation of Lamu coal should be phased and the plant to constitute smaller units of 150MW each to minimise requirement of primary reserves.